Welcome to our live ASX coverage for Monday, July 13. Expect a high volume of posts pre-market and more periodic updates throughout the day. We’ll be wrapping the blog up around 2:00 pm AEST. Let us know how we can make it even better.

ASX 200 dips as tech, materials and healthcare drag

[2:00 pm] Another dicey day for markets, with the ASX 200 currently down 0.2%, held up by large cap banks, retailers and telcos. The larger end of town is faring better, with the S&P/ASX 20 up a solid 0.13%, while things get worse the smaller you go, with the S&P/Emerging Companies index down 1.7% to a one-month low.

|

BHP |

BHP |

-0.38% |

$58.06 |

|

CBA |

Commonwealth Bank |

0.49% |

$169.69 |

|

RIO |

Rio Tinto |

-0.36% |

$163.90 |

|

WBC |

Westpac Banking Corporation |

0.42% |

$36.70 |

|

NAB |

National Australia Bank |

0.57% |

$39.84 |

|

ANZ |

ANZ Group |

0.90% |

$36.38 |

|

WES |

Wesfarmers |

1.60% |

$91.14 |

|

MQG |

Macquarie Group |

-0.36% |

$253.59 |

|

GMG |

Goodman Group |

-0.47% |

$29.83 |

|

CSL |

CSL |

-1.29% |

$121.31 |

|

FMG |

Fortescue |

1.38% |

$18.73 |

|

WDS |

Woodside Energy Group |

0.65% |

$29.24 |

|

TLS |

Telstra Group |

1.73% |

$4.99 |

|

WOW |

Woolworths Group |

-0.55% |

$39.94 |

|

TCL |

Transurban Group |

1.20% |

$14.80 |

Data as at 1:58 pm | Source: Market Index

Tech (-2.3%), materials (-0.9%) and healthcare (-0.8%) are leading the downside. While the face value moves aren’t great, the indices are still holding up. Tech has had its ups and downs in recent months and is now back to mid-April levels, Materials is giving back some of last Friday’s 2.6% bounce, and healthcare is in the midst of a pullback after rallying 23% between 3 June and 9 July. So not really destabilising moves to the downside. That said, the market has been awfully choppy in recent weeks and it’s difficult to find any short-term conviction, with stocks and sectors whipping back and forth.

That’s all for today. S&P 500 and Nasdaq futures are down 0.48% and 1.08% respectively, while Brent is still hovering session highs, up 5.2% to US$79.15 a barrel.

Gold stocks broadly lower

[1:40 pm] Gold prices are trading sharply lower on Monday, down 1.5% to US$4,058/oz, as the US-Iran escalation places upward pressure on bond yields and the US dollar. The S&P/All Ords Gold Index is currently down 2.0% after bouncing 2.6% last Friday.

|

SBM |

St. Barbara |

-4.3% |

$0.45 |

-11.8% |

-21.7% |

|

BC8 |

Black Cat Syndicate |

-4.2% |

$0.91 |

-6.2% |

-25.1% |

|

RSG |

Resolute Mining |

-4.2% |

$0.91 |

-10.3% |

-25.7% |

|

CMM |

Capricorn Metals |

-3.7% |

$12.82 |

-9.2% |

-8.5% |

|

BGL |

Bellevue Gold |

-3.0% |

$1.28 |

-5.6% |

-24.6% |

|

NST |

Northern Star Resources |

-3.0% |

$19.88 |

-9.7% |

-19.1% |

|

MEK |

Meeka Metals |

-2.7% |

$0.11 |

-7.0% |

-60.4% |

|

RMS |

Ramelius Resources |

-2.6% |

$2.96 |

-8.1% |

-27.6% |

|

PNR |

Pantoro Gold |

-2.6% |

$2.04 |

-15.6% |

-58.5% |

|

OBM |

Ora Banda Mining |

-2.5% |

$1.09 |

-9.0% |

-28.6% |

|

WGX |

Westgold Resources |

-2.2% |

$4.66 |

-8.0% |

-26.1% |

|

EMR |

Emerald Resources |

-2.1% |

$5.23 |

-8.2% |

-16.7% |

|

PRU |

Perseus Mining |

-2.0% |

$4.84 |

-6.9% |

-12.2% |

|

EVN |

Evolution Mining |

-1.8% |

$11.42 |

-10.8% |

-9.2% |

|

AMI |

Aurelia Metals |

-1.8% |

$0.28 |

-6.8% |

12.2% |

|

ALK |

Alkane Resources |

-1.4% |

$1.40 |

-3.8% |

4.9% |

|

NEM |

Newmont |

-0.9% |

$134.66 |

-6.4% |

-10.3% |

|

RRL |

Regis Resources |

-0.8% |

$6.47 |

-3.4% |

-14.0% |

|

VAU |

Vault Minerals |

-0.1% |

$4.87 |

-3.9% |

-10.6% |

|

CYL |

Catalyst Metals |

1.0% |

$5.82 |

-4.7% |

-21.1% |

|

GMD |

Genesis Minerals |

2.3% |

$5.80 |

-2.0% |

-19.0% |

Another rough day for copper miners

[1:36 pm] Copper prices are trading 1.1% lower on Monday to US$6.22/lb, driving broad weakness across most copper names. Copper prices have fallen around 7.2% from 2 June record highs of US$6.71/lb, but still up 8.5% year-to-date. Despite prices trading around flattish over the past week, plenty of copper names are down 5-10% in the past week.

|

AR1 |

Austral Resources |

-4.6% |

$0.06 |

-13.9% |

8.8% |

|

FFM |

Firefly Metals |

-4.4% |

$1.72 |

-10.6% |

-16.5% |

|

HCH |

Hot Chili |

-3.7% |

$1.56 |

-20.3% |

11.9% |

|

SFR |

Sandfire Resources |

-3.3% |

$18.20 |

-5.9% |

1.3% |

|

MC2 |

Marimaca Copper |

-3.0% |

$7.51 |

-10.6% |

-39.9% |

|

29M |

29Metals |

-2.0% |

$0.24 |

-11.1% |

-54.4% |

|

CSC |

Capstone Copper Corp |

-1.4% |

$12.86 |

-4.8% |

-15.2% |

|

CYM |

Cyprium Metals |

-1.2% |

$0.43 |

-7.6% |

-19.7% |

|

RIO |

Rio Tinto |

-0.7% |

$163.35 |

-4.7% |

11.3% |

|

BHP |

BHP Group |

-0.6% |

$57.91 |

-4.1% |

27.2% |

|

HGO |

Hillgrove Resources |

0.0% |

$0.06 |

8.8% |

29.2% |

|

CPM |

Cooper Metals |

0.0% |

$0.06 |

-10.4% |

7.1% |

|

AIS |

Aeris Resources |

1.4% |

$0.38 |

-1.3% |

-37.5% |

China sets up new investment vehicle to tighten grip on overseas minerals

[1:25 pm] China has established a Beijing-backed mining investment firm to bolster its control of overseas resources as the US and Europe push to break its dominance of critical mineral supply chains.

-

Guangyan International Investment (also known as Vast Rock) will sit within a broader NDRC-led effort, offering direct equity investment plus compliance, risk-management and market advice

-

Beijing aims to standardise its process for international metals deals and is encouraging miners to bring in partners rather than take full ownership as costs and political risks rise

-

Chinese companies have spent over US$100bn on strategic outbound mining M&A over two decades, with copper, iron ore and gold most sought after, per Bain & Co

-

Working with Guangyan is not mandatory, and larger companies may resist sharing information, as some have with China Mineral Resources Group in iron ore

-

Producer nations are demanding more, with Congo controlling cobalt exports, Guinea eyeing bauxite limits and Simandou processing, and Zimbabwe pressing for lithium refining investment

-

The US is courting allies for an alternative supply chain, including a Congo partnership granting US investors preferential access to copper, cobalt, lithium and tantalum

-

Separately, China has told some major refiners to keep fuel production high to protect domestic consumers as Persian Gulf strikes again threaten oil shipments

Source: Bloomberg

Australia’s $4.4 trillion super system draws Trump’s attention

[1:24 pm] Australia’s compulsory superannuation system, the world’s fourth-largest retirement pool, has caught Donald Trump’s eye as a potential template for reforming the US system.

-

The system holds $4.4 trillion (US$3.1 trillion) in assets, equal to roughly 150% of GDP and forecast to approach 250% by 2060, with assets tipped to triple to as much as $10 trillion within two decades

-

Employers must pay 12% of salary into predominantly defined-contribution accounts, up from 3% when compulsory super was introduced in 1992

-

Trump has directed Bessent and Lutnick to study the model, with BlackRock’s Larry Fink a long-time champion of its compulsory design

-

About half of all capital is now invested offshore, with around a third in global equities and a fifth in unlisted assets such as infrastructure and private credit

-

AustralianSuper is the largest fund at $410bn, ahead of Australian Retirement Trust at $370bn and Aware Super at $235bn

-

Australia ranks seventh in the 2025 Mercer CFA Institute Global Pension Index, ahead of the UK at 12th and the US at 30th, with the US Social Security trust fund projected to deplete in 2032

Source: Bloomberg

Morgan Stanley stays Overweight ASX resources, sees recent pullback as a rotation opportunity

[12:48 pm] Morgan Stanley retains its overweight on ASX resources after a sharp six-week drawdown, preferring copper, uranium and gold as commodity drivers turn more stock-specific.

-

ASX Resources is up about 43% over 12 months, outperforming Banks by about 39%, but has fallen 10.4% over the past six weeks as energy prices, USD strength and spot volatility weighed

-

The sector team views the recent weakness as a pullback to rotate into rather than a cycle inflection, retaining Materials and Energy overweights against banks, housing and consumer exposures facing a domestic slowdown

-

Preference order is copper, uranium, gold and thermal coal, with aluminium and iron ore least preferred

-

Copper is the top pick, with a 4Q26 COMEX forecast of US$6.85/lb and LME US$14,250/t, supported by tight mine supply and data centres driving 30% of 2026 demand growth

-

Uranium term prices hit an all-time high of US$95.50/lb, with a forecast 13.5Mlb 2026 deficit and a 4Q26 spot forecast of US$95/lb

-

Gold is forecast at US$4,450/oz in 4Q26, underpinned by 700t of modelled central bank buying, though the recovery is seen as slower as ETF demand moderates

-

Iron ore is expected to drift to the lower end of its US$90-110/t range, with a 4Q26 forecast of US$92/t, as seaborne supply improves and Simandou ramps

-

The US Fed path remains the key macro risk, with MS economists expecting a hold through 2026 before 25bp cuts in March and June 2027

Auction clearances rebound to seven-week high as low volumes support market

[12:47 pm] Auction clearance rates lifted to their highest in seven weeks as reduced listings constrained buyer choice and the market steadied after post-budget shocks.

-

Preliminary combined capitals clearance rate hit 54.8%, up from last week’s 49.8% (revised to 46% on final numbers), per Cotality

-

Auction volumes fell 8.7% week-on-week to 1,318 properties amid winter school holidays and cautious vendors

-

Sydney cleared 57.5% of 452 properties, its highest in 10 weeks, while Melbourne cleared 56.2% of 585, a four-week high

-

Brisbane rose to 43% from 23%, and Adelaide to 59.1% from 45.7%

-

Agents noted quality homes still achieving strong results while lower-grade stock is judged harshly, with buyer urgency and FOMO evaporating post-budget

-

Market remains pressured by rate hikes, global instability, generational property tax changes and cost-of-living strain

Top ASX 200 gainers and losers at noon

[12:42 pm] Here are the top large cap winners and losers at noon. Not much change since the morning update, with Mesoblast trading around session highs thanks to a broker update (Bell Potter upgraded to Speculative Buy with $4.45 target). Meanwhile, a broad list of gold, uranium, lithium and copper names lag.

|

MSB |

Mesoblast |

5.36% |

$2.36 |

|

SIG |

Sigma Healthcare |

3.37% |

$2.92 |

|

GMD |

Genesis Minerals |

3.00% |

$5.84 |

|

ALD |

Ampol |

2.66% |

$36.22 |

|

4DX |

4DMedical |

2.53% |

$4.06 |

|

ARB |

ARB Corp |

2.37% |

$17.95 |

|

JDO |

Judo Capital |

2.17% |

$0.94 |

|

NEC |

Nine Entertainment Co |

2.12% |

$0.97 |

|

CYL |

Catalyst Metals |

2.08% |

$5.88 |

|

SUL |

Super Retail Group |

1.94% |

$13.16 |

|

KCN |

Kingsgate |

-11.82% |

$4.40 |

|

SLX |

Silex Systems |

-5.96% |

$5.36 |

|

LTR |

Liontown |

-5.70% |

$1.41 |

|

VUL |

Vulcan Energy Resources |

-5.57% |

$2.71 |

|

RMD |

Resmed |

-5.53% |

$28.37 |

|

ASB |

Austal |

-4.57% |

$3.55 |

|

ILU |

Iluka Resources |

-4.48% |

$6.39 |

|

FFM |

Firefly Metals |

-4.33% |

$1.72 |

|

MIN |

Mineral Resources |

-4.29% |

$57.14 |

|

AGL |

AGL Energy |

-4.27% |

$8.08 |

Xero CEO sells entire shareholding for $2.2m amid pay reset talks

[11:40 am] Xero CEO Sukhinder Singh Cassidy has sold her entire ordinary shareholding, citing personal tax obligations, as the board seeks investor support for a new pay package.

-

Sold 29,608 shares at $74.00 for $2,19m, disposing of her entire ordinary holding, citing management of personal tax obligations

-

Follows more than $4m of share sales a month earlier, taking recent disposals above $6m

-

Retains 171,381 restricted stock units and 1,038,308 unlisted options after the sale, but no current equity

-

Her options are struck at $171.11 against a current share price of $70.86, down 57% over the past year, leaving them almost worthless

-

Chair David Thodey has been meeting investors to secure support for resetting her pay to be less exposed to the share price, per the AFR

Company page: Xero (XRO)

Brent jumps 5% as US-Iran strikes intensify and Hormuz status stays disputed

[11:41 am] Brent crude rose more than 5% as fresh US-Iran strikes and conflicting claims over the Strait of Hormuz revived supply disruption fears.

-

Brent crude up 5.3% to $79.22 a barrel on concerns over potential supply disruptions

-

US struck Iran for the fourth time in about a week, following Saturday’s bombardment of around 140 targets ordered by Trump, aimed at degrading Iran’s ability to attack Hormuz shipping

-

Iran declared Hormuz closed «until further notice», but CENTCOM, Trump and the Joint Maritime Information Center maintain the waterway is open, with the southern route still transitable

-

Axios reported around 20 commercial vessels transited Hormuz in coordination with the US military, though the JMIC called the security threat «severe» with visible traffic near zero

-

The UK, France and Germany issued a joint statement condemning Iran’s attacks on shipping and calling for a return to the ceasefire and peace talks

Tech stocks broadly lower

[11:36 am] The S&P/ASX 200 Tech Index is down 2.0%, hitting a fresh two-week low, with most large cap names like Wisetech, NextDC and Xero down 2-3%.

|

BVS |

Bravura Solutions |

-6.4% |

$2.21 |

10.5% |

-14.0% |

|

SDR |

Siteminder |

-4.3% |

$3.56 |

-9.6% |

-41.9% |

|

XRO |

Xero |

-3.9% |

$70.53 |

-2.0% |

-38.1% |

|

WBT |

Weebit Nano |

-2.8% |

$7.61 |

-3.7% |

52.2% |

|

WTC |

Wisetech Global |

-2.8% |

$33.06 |

0.9% |

-51.7% |

|

NXL |

Nuix |

-2.3% |

$1.26 |

5.4% |

-30.4% |

|

NXT |

NextDC |

-2.2% |

$13.64 |

0.7% |

10.7% |

|

DDR |

Dicker Data |

-1.9% |

$11.76 |

-0.3% |

14.3% |

|

AD8 |

Audinate Group |

-1.7% |

$2.29 |

-2.6% |

-43.6% |

|

TNE |

Technology One |

-1.6% |

$30.30 |

-0.6% |

9.9% |

|

DTL |

Data#3 |

-1.5% |

$9.35 |

0.1% |

4.2% |

|

MAQ |

Macquarie Technology Group |

-1.4% |

$64.77 |

-0.3% |

-3.3% |

|

IFT |

Infratil |

-1.3% |

$12.75 |

-1.9% |

33.1% |

|

360 |

Life360 |

-1.1% |

$25.40 |

-7.3% |

-21.2% |

|

CDA |

Codan |

-1.0% |

$42.86 |

-2.8% |

50.8% |

|

IRE |

Iress |

-0.6% |

$6.27 |

-2.3% |

-25.2% |

|

MP1 |

Megaport |

-0.2% |

$20.03 |

5.4% |

76.5% |

|

PPS |

Praemium |

0.0% |

$0.73 |

5.8% |

-8.2% |

|

OCL |

Objective Corporation |

0.0% |

$6.96 |

2.7% |

-57.9% |

|

PME |

Pro Medicus |

0.7% |

$198.45 |

-4.6% |

-10.1% |

|

DGT |

Digico Infrastructure Reit |

0.8% |

$2.55 |

6.3% |

-8.6% |

|

CAT |

Catapult Sports |

1.0% |

$3.42 |

13.8% |

-17.9% |

|

HSN |

Hansen Technologies |

1.2% |

$4.25 |

-3.4% |

-19.5% |

Macquarie turns cautious on Australian consumer, pivots selectively into discretionary

[10:53 am] Macquarie says the consumer sector now screens expensive across both staples and discretionary, and expects a cyclical slowdown in FY27 before conditions progressively improve.

-

Preferred names are Sigma Healthcare on Health & Beauty, JB Hi-Fi on structural tailwinds, and Bega Cheese on long-term growth

-

Least preferred are Endeavour on cost pressure, Inghams on competition, and Woolworths post its re-rate

-

Household spend growth is expected to slow to 1.5% year-on-year in FY27, with select discretionary categories yet to feel the brunt of weaker conditions, likely showing in the December half

-

Volatile CY26 to date has seen the market pivot to defensives, with the Staples Index outperforming by about 12%, led by Woolworths up 39%, while Discretionary is now only underperforming by about 3%

-

The market is pricing roughly half an RBA hike by end-CY27 after three rate hikes this year, though conditions are skewed to improvement into CY27

-

Upgrades conviction on Sigma (outperform) on medium-term consensus upside, and lifts preference for JB Hi-Fi (outperform) as structural tailwinds persist

-

Downgrades Woolworths to underperform on an overestimated recovery pace, and retains underperform on Endeavour and Inghams on top-line softness and margin downside

UBS stays neutral on Telcos ahead of August results, flags Enterprise dilution risks

[10:52 am] UBS expects Telstra and TPG to broadly meet earnings and dividend expectations at their August results, but sees softening industry trends and mobile ARPU dilution risks.

-

Reiterates neutral on Telstra (PT $5.30) and TPG (PT $3.97), viewing valuations as relatively full at 7.6x and 5.8x forward EBITDA and 4.4% and 5.3% dividend yields versus global peers on around 7x

-

Postpaid net adds likely flattish as the market matures, with activity concentrated at the value end, though mobile price rises should be captured

-

Mobile price hikes continue, with Vodafone lifting front book postpaid pricing $5/month (+9% year-on-year), following Telstra +$4 in May (+6%) and Optus +$5 in June (+9%)

-

Blended mobile ARPU dilution risk from rising Enterprise competition as TPG seeks share, plus TPG signing three new MVNO contracts (Zmobile, Spacetalk ~58k subs, Swoop 135k subs), lifting UBS’s TPG MVNO forecast by about 193k subs over 12 months

-

Potential upside from further cost-out and productivity initiatives, though persistent Australian inflation could pose near-term downside

Coles slides on report of ~$4bn Greencross pet acquisition

[10:44 am] Coles is reportedly close to acquiring pet care group Greencross for more than $4 billion, according to The Australian. The stock is down 2.1% at the time of writing to $23.04.

-

The deal could be announced as soon as this week at a price above $4bn (around US$2.8bn) including debt, according to the Australian

-

The pivot into vet and pet care marks an odd diversification for the grocery group and has rattled investors, though rival Woolworths took a 55% stake in Petspiration Group for $586m in December 2022, citing growth across pet daycare, nutrition and grooming

-

Coles held $598m in cash as at 4 January 2026, so the acquisition will likely require debt or a capital raising

Company page: Coles Group (COL)

AGL tumbles on broker downgrade

[10:37 am] Macquarie has downgraded AGL to underperform, warning a structurally oversupplied power market will defer earnings recovery to FY31.

-

Price target cut to $7.75 from $8.83, reflecting the deferral of higher power prices to FY31 from FY29

-

Rating lowered to Underperform from Neutral, with Macquarie arguing AGL’s downgrade cycle is not fully reflected in consensus

-

Power prices sit at 5-year lows with weak forward curves, as LTESA and CIS capacity add to a structurally oversupplied system

-

Coal exiting the market is central to any price recovery, but data centre demand may push that exit out 12-24 months by absorbing new renewable capacity

-

Power price normalisation deferred to FY31 from FY29 on growing expectations of delayed coal closures such as Eraring, cutting valuation by about $0.90

-

Key upside risks are on-schedule coal closures driving a price rebound, or unplanned coal outages lifting volatility, which would favour gas and battery portfolios

Company page: AGL Energy (AGL)

ASX 200 lower as Utilities, Tech and Staples dip

[10:34 am] The S&P/ASX 200 is currently down 0.15% despite a slightly positive, weighed by:

-

Utilities (-2.1%) sharply lower, with AGL shares down 4% after Macquarie downgraded the stock to underperform, warning a structurally oversupplied power market will defer earnings recovery to FY31

-

Tech (-1.4%) broadly lower, led by names like Xero (-1.2%), NextDC (-1.2%), Dicker Data (-2.2%) and Aura (-2.4%)

-

Staples (-1.2%) hit by weakness in Coles (-2.5%) after The Australian reported the company is expected to announce a deal to acquire Greencross as soon as this week (at a high price of ~$4bn, which will likely require a capital raising)

S&P/ASX 200 sectors (Source: Market Index)

Kingsgate hit by Chatree plant failure days after meeting FY26 guidance

[10:26 am] Kingsgate shares are down 15% after the company shut down Plant 1 at its Chatree Gold Mine following a mechanical failure, just after confirming it met full-year production guidance.

-

Plant 1 ball mill was taken offline late on 10 July after operators identified elevated bearing temperatures, with the operational and financial impact still being assessed

-

Chatree produced 20,163 ounces of gold in the June quarter, taking FY26 output to 86,078 ounces and meeting guidance

-

FY26 gold production rose 15% on FY25, reflecting the first full year of steady-state operations since the Chatree restart

-

June quarter silver output of 220,078 ounces lifted FY26 silver production to 766,009 ounces, up 22% on FY25

-

Held $179m in cash and bullion at 30 June, including $26m of restricted cash

-

CEO Jamie Gibson pointed to the balance sheet supporting the interim dividend and the acquisition of royalty and water rights from Inversiones Anglo American Norte

Company page: Kingsgate Consolidated (KCN)

Top ASX 200 gainers and losers

[10:25 am] Here are the top large cap gainers and losers in early trade.

|

MSB |

Mesoblast |

6.70% |

$2.39 |

|

4DX |

4DMedical |

5.56% |

$4.18 |

|

ARB |

ARB Corp |

3.88% |

$18.21 |

|

GMD |

Genesis Minerals |

2.91% |

$5.84 |

|

SIG |

Sigma Healthcare |

2.48% |

$2.89 |

|

SLX |

Silex Systems |

2.46% |

$5.84 |

|

CNI |

Centuria Capital Group |

2.29% |

$1.79 |

|

KAR |

Karoon Energy |

2.26% |

$1.45 |

|

CYL |

Catalyst Metals |

2.08% |

$5.88 |

|

MI6 |

Minerals 260 |

1.61% |

$0.63 |

|

KCN |

Kingsgate |

-15.13% |

$4.24 |

|

RMD |

Resmed |

-4.30% |

$28.74 |

|

AGL |

AGL Energy |

-3.91% |

$8.11 |

|

RSG |

Resolute Mining |

-3.47% |

$0.92 |

|

XRO |

Xero |

-2.68% |

$71.43 |

|

GGP |

Greatland Resources |

-2.56% |

$10.87 |

|

FFM |

Firefly Metals |

-2.50% |

$1.76 |

|

PNR |

Pantoro Gold |

-2.39% |

$2.04 |

|

NST |

Northern Star Resources |

-2.32% |

$20.01 |

|

COL |

Coles Group |

-2.29% |

$23.02 |

BHP explores $2bn sale of Chilean desalination plant and power lines

[9:46 am] BHP is exploring the sale of a Chilean desalination plant and electricity transmission assets that could fetch a combined $1.5 billion to $2 billion, extending its push to monetise non-core infrastructure and fund its copper business.

-

The transmission lines are expected to raise about $1 billion to $1.3 billion and the desalination plant roughly $500 million to $700 million

-

The process is early-stage with no final decision made, and valuation, timing and structure are still under discussion

-

The Puerto Coloso plant serves Escondida, the world’s largest copper mine, and is one of the biggest reverse osmosis plants globally

-

Any buyer would likely enter long-term service agreements with BHP, providing stable cash flows

-

The move is part of BHP’s plan to unlock up to $10 billion from infrastructure, by-products and other non-core assets

-

BHP has already agreed to sell a 49% stake in transmission assets serving its WA iron ore operations and signed a $4.3 billion silver streaming deal tied to Peru’s Antamina mine

-

The company has sharpened its focus on copper and potash, exiting petroleum, shrinking coal and funding growth at Escondida and the Vicuña district in Argentina

Source: Bloomberg

Mayne Pharma investors float break-up as shares languish post-Cosette

[9:32 am] Some Mayne Pharma shareholders are pushing for a break-up of the drugmaker, arguing its Adelaide and North Carolina manufacturing plants could fetch more sold separately than the current share price implies, the AFR reports.

-

Investor sources say Mayne should explore splitting and selling its Salisbury South (Adelaide) and Greenville (North Carolina) facilities to the highest bidder

-

The $233 million company’s board is not known to be preparing a sale or to have received proposals

-

The Adelaide plant, freshly upgraded in an $18 million modernisation, may be a tricky buy for offshore parties after Treasurer Jim Chalmers blocked Cosette’s $672 million bid on national interest grounds, though the US operations could attract a local pharma buyer

-

MST’s Andrew Goodsall values Mayne at $3.73 to $5.77 per share on a sum-of-the-parts basis, against a last close of $2.87.

-

Offshore hedge funds hold about 20% of the register, including Rubric Capital (5.36%), Funicular Funds (9.90%) and Trium Capital (5.02%), with shares having bottomed at $2.04 in March versus $7.24 when the deal was announced.

-

Cosette’s appeal is expected to wrap up in the next few weeks, potentially clearing the way for Mayne, advised by Jefferies, to act.

Source: AFR

oOh!media fields three takeover bids as buyout race narrows to binding talks

[9:29 am] oOh!media has received reconfirmed non-binding takeover proposals from three private capital suitors, topping out at $1.65 per share, and will move to binding negotiations over the next four weeks.

-

Pacific Equity Partners, I Squared Capital and Oaktree Capital Management each reconfirmed their non-binding indicative offers on 10 July, with conditions unchanged from earlier disclosure.

-

The proposals are for at least $1.60 per share, with the highest at $1.65.

-

The board intends to keep engaging with all three parties to allow confirmatory diligence and negotiation of binding documentation, a process expected to take up to four weeks.

-

There is no certainty any proposal will become a binding offer, and the board recommends shareholders take no action at this stage.

OML shares closed at $1.475 last Friday, so the highest $1.65 bid represents an 11.8% premium to the last close, or a ~94% premium to the 28-Apr close (the day before the first offer emerged).

Company page: oOh!media (OML)

Count clears ACCC hurdle for Oracle Group deal and secures CBA funding

[9:24 am] Count has confirmed the ACCC does not require notification of its Oracle Group acquisition, clearing the way for completion in the coming weeks alongside an enhanced debt facility with CBA.

-

The ACCC confirmed, following Count’s waiver application, that the Oracle Group acquisition is not required to be notified.

-

Completion is expected in the coming weeks, subject to the conditions precedent outlined in the 31 March 2026 investor presentation.

-

Count has entered an enhanced CBA debt facility comprising a $77.0 million three-year acquisition facility, a $33.0 million credit-approved accordion facility and a $6.6 million working capital facility.

-

The new facility replaces the group’s existing Westpac facilities and funds the acquisition, refinances existing debt and supports growth.

-

Any earn-out consideration is expected to be funded through future operating cash flows and debt drawdowns.

Company page: Count (CUP)

Orthocell posts record revenue as US Remplir rollout accelerates

[9:23 am] Orthocell delivered record June-quarter revenue of $3.8 million and record FY2026 revenue of $13.2 million, driven by Remplir adoption in Australia and building US commercial traction.

-

June quarter revenue rose 20% on the March quarter and 36% on the prior corresponding quarter to $3.8 million.

-

FY2026 revenue climbed 44% to $13.2 million, underpinned by Remplir and Striate+ sales growth.

-

International Remplir sales now account for over 9% of quarterly revenue, with distributors appointed in Canada and Thailand and UK/EU sales expected in 1H CY2027.

-

US Value Analysis Committee approvals rose 38% to 44, opening access to 151 hospitals, with approval also secured across the Department of Defense and Veterans Affairs networks covering 221 medical centres.

-

Hospitals purchasing Remplir rose 27% to 70 and surgeons using it rose 55% to 76 over the quarter.

-

Funds available were $44.1 million at 30 June, comprising $9.4 million cash and $34.7 million in security and term deposits, with quarterly operating cash burn of $3.6 million.

Company page: Orthocell (OCC)

FleetPartners upgrades FY26 new business guidance as NBW momentum builds

[9:10 am] FleetPartners has lifted its FY26 new business writings forecast to high-single-digit growth, citing an 8% year-to-date rise despite a softer used vehicle market weighing on end-of-lease income.

-

New business writing (NBW) grew 8% YTD, with $246m written in 3Q26, up 24% on 3Q25

-

FY26 NBW outlook was upgraded from marginal growth to high-single-digit growth, with the June pipeline running 27% above the 1H26 average

-

Assets Under Management or Financed (AUMOF) rose 6% year on year to $2.44 billion and Core income grew 7% YTD, with AUMOF on track for mid-single-digit FY26 growth

-

End-of-lease profit per unit fell to $4,951 in 3Q26 as the group held back inventory to protect pricing, cutting units sold 31% versus 2Q26

-

Novated leasing grew 20% YTD, helped by EV demand and the Remunerator acquisition.

-

FY26 operating expenses are guided to $98.5-$99.5m, with a 60% to 70% payout ratio expected to be fully franked

-

$8m of the up-to-$20m buy-back announced in March has been completed, with Australian cash tax payments resuming in 2H26 as carried-forward losses are exhausted

Company page: FleetPartners Group (FPR)

Clinuvel wins Health Canada approval for SCENESSE in EPP

[9:08 am] Clinuvel has secured a Notice of Compliance from Health Canada for SCENESSE to prevent phototoxicity in adults with erythropoietic protoporphyria, opening a fourth major market for the drug.

-

The NOC grants Clinuvel the right to market SCENESSE in Canada, following approvals in Europe in 2014, the US in 2019 and Australia in 2020

-

SCENESSE remains the only EPP treatment to hold marketing authorisation from any regulator worldwide

-

Five Canadian Specialty Centers are already trained and accredited and have treated EPP patients under special access arrangements

-

EPP affects an estimated 5,000 to 10,000 people globally, including about 1 in 140,000 in Canada

-

Over 21,000 doses of SCENESSE have been administered worldwide, with the longest-treated patients receiving up to 20 years of continuous therapy

Company page: Clinuvel Pharmaceuticals (CUV)

GQG Partners posts US$3.2 billion of June outflows as FUM slips to US$156 billion

[9:06 am] GQG Partners recorded net outflows of US$3.2 billion in June and US$15.1 billion for the first half, dragging total funds under management down to US$156.0 billion.

-

Total FUM fell to US$156.0 billion at 30 June, down from US$163.3 billion a month earlier, a decline of about 4.5%

-

June net outflows of US$3.2 billion were compounded by negative investment performance of US$4.1 billion

-

International was the largest drag, ending the month at US$70.1 billion after US$1.6 billion of outflows and US$1.6 billion of negative performance

-

For the half year, net outflows totaled US$15.1 billion, partly offset by positive investment performance of US$7.2 billion

-

All four strategies saw first-half outflows, led by Emerging at US$5.2 billion and International at US$4.7 billion

-

GQG said its strategies underperformed benchmarks in the first half but delivered positive absolute returns, with double-digit net returns over three years

Company page: GQG Partners (GQG)

Rox Resources fully permitted at Youanmi as mill construction begins

[8:59 am] Rox Resources has secured its final major environmental approval for the Youanmi gold mine, clearing the way for processing plant construction and keeping first gold on track for mid-2027.

-

The Works Approval covers the processing plant, tailings storage facility, wastewater treatment, power station and associated infrastructure, leaving the project fully permitted

-

EPC contractor Interquip has mobilised to site and begun construction on the 1.0Mtpa processing plant, with first steel due this month

-

The historic Youanmi Decline is advancing and the high-grade Pollard Decline has started, giving three separate mining fronts

-

United North mining is running ahead of the DFS, with 339m of advance in June and ROM stockpiles building toward a 190,000t at 3.3g/t target for commissioning

-

Underground diamond drilling has started at United North, focused initially on infill to improve geological control

-

Cash stood at $152.7 million at 30 June, down $47.7 million over the quarter as mining and construction ramped up, with $350 million in debt facilities available to draw in 2H CY2026

Company page: Rox Resources (RXL)

Terra Metals extends Southwest sulfide discovery to surface at Dante

[8:57 am] Fresh drilling has grown Terra Metals’ Southwest PGM-copper-nickel discovery to more than 950m of strike, with a near-surface 157m intercept lifting confidence in a potential low-strip starter pit.

-

The Southwest Main Sulfide Corridor now spans over 950m of strike, about 700m of width and at least 750m down-dip, and remains open in all directions

-

The discovery sits entirely outside the existing 148Mt Dante mineral resource, marking a new growth avenue within the Jameson Layered Intrusion

-

The company is targeting a maiden Southwest resource in late 2026, ahead of metallurgical test work and a potential pre-feasibility study

Company page: Terra Metals (TM1)

Vault to terminate Regis deal and sign with Genesis after matching period lapses

[8:56 am] Vault Minerals will terminate its scheme with Regis Resources and enter a definitive agreement with Genesis Minerals after Regis declined to match Genesis’ superior proposal.

-

Regis confirmed earlier today it will not submit a counter proposal under its matching rights, with the matching right period set to expire later today

-

Vault has until 7:00 am AWST tomorrow, 14 July, to terminate the Regis SID and accept the binding Genesis Proposal

-

Vault intends to terminate the Regis deal and sign a definitive agreement with Genesis as soon as it is able

-

A break fee of about $50.7 million becomes payable to Regis on termination

Company page: Vault Minerals (VAU)

Global EV demand rises for fourth month as Europe offsets China and US weakness

[8:52 am] Global electric vehicle sales rose again in June, with record European growth more than compensating for declines in China and North America.

-

Battery-electric and plug-in hybrid registrations rose 7% year-on-year to 2 million in June, with first-half volumes up 2%, per Benchmark Mineral Intelligence

-

Europe registrations jumped 31% to about 530,000 units, a record for June, and remain the main engine of global EV growth

-

China registrations fell 11% to around 1 million vehicles

-

North America registrations fell 13% following the end of US EV tax credits

-

Chinese automakers continue expanding overseas amid weaker domestic demand

Source: Reuters

Fuel prices squeeze consumers even as crude retreats

[8:50 am] Gasoline, diesel and jet fuel prices are climbing even as crude oil eases, a rare divergence driven by refinery bottlenecks and supply shocks that threatens to keep inflation sticky.

-

The gap between refined product prices and raw crude has hit a record in the US and other regions, even as oil benchmarks have all but erased the Iran war spike

-

Russia, the world’s second-largest diesel exporter at 11% of global shipments, has banned diesel exports after Ukrainian attacks on its refineries, sending Brazil and Turkey into a bidding war for non-Russian supply

-

Refined product flows through the Strait of Hormuz have fallen to near 1 million barrels a day from about 5 million before the US attacked Iran, per Citigroup

-

US distillate stockpiles sit just off all-time seasonal lows and are drawing when they typically build, while European refiners face heatwave output cuts of up to 15%

-

China authorised larger fuel exports this week for the first time since March, though traders warn Middle East tensions could prompt Beijing to pull back

Source: Bloomberg

China drops five-year urban jobs target for first time in decades as AI looms

[8:50 am] China omitted a numerical urban job creation target from its 2026-2030 plan for the first time since at least the 1990s, signalling rising uncertainty over AI-driven displacement.

-

The five-year plan pledges to keep new urban jobs at a «considerable scale» over 2026-2030, with annual targets now set flexibly year by year

-

It is the first medium-term plan since at least the 1990s to omit a headline urban jobs number, which last stood at more than 55 million for the previous five years

-

Beijing said it will address the employment impact of AI and other new technologies alongside a shifting external environment, a likely nod to trade barriers

-

The March work report had targeted more than 12 million new urban jobs for 2026 alongside a 4.5% to 5% growth goal, the most modest since 1991

Source: Bloomberg

Delta slips despite profit beat and reaffirmed guidance

[8:47 am] Delta topped earnings estimates and revived its full-year profit forecast on strong premium and corporate demand, but shares fell on fuel cost pressure and fare structure concerns.

-

Adjusted EPS of $1.56 vs $1.51 ests (3% beat)

-

Revenue up 14% year-on-year, with capacity up just 1%

-

Premium revenue up 17% year-on-year, loyalty and related revenue up 19%, and American Express payments up 16% to US$2.4bn

-

Reaffirmed 2026 adjusted EPS guidance of $6.50 to $7.50, restoring the January forecast it omitted in April, but declined to guide for 2027

-

Adjusted fuel expense up 77% year-on-year to US$4.4bn

-

CEO Ed Bastian said airfares are unlikely to decline as carriers recover higher fuel costs, with fuel still up 50%

-

Shares fell 1.8%

A very interesting comment from management: “We delivered $1.4 billion in pre-tax profit while absorbing the highest quarterly fuel expense in our history, reflecting broad demand strength, growing brand preference and momentum across our diversified revenue base.”

US steps up Iran strikes as Hormuz status flips to closed

[8:44 am] The US has hit Iran four times in a week and both sides now issue contradictory claims over whether the Strait of Hormuz is open, keeping oil markets on edge.

-

US Central Command says weekend strikes hit around 140 Iranian military sites, taking the total across the week’s rounds to more than 300 targets, ordered by Trump in response to Iranian attacks on commercial shipping

-

Iran declared Hormuz closed «until further notice», but CENTCOM, Trump and the US Navy insist the waterway remains open, with the JMIC saying the southern route is still transitable

-

Tracking data showed traffic reduced to a trickle on Sunday, with only two oil-products tankers seen approaching

-

Iran retaliated against US assets across the Gulf, striking bases in Jordan and Qatar and hitting a Kuwait Oil Co drilling rig, with only minor damage and a handful of injuries reported

-

The escalation casts doubt over the June US-Iran memorandum of understanding, which UN ambassador Mike Waltz said has «broken down», though he confirmed technical talks continue

-

Oman has drafted a proposal to manage Hormuz transits via two separately controlled routes, with Pakistan urging all sides to de-escalate

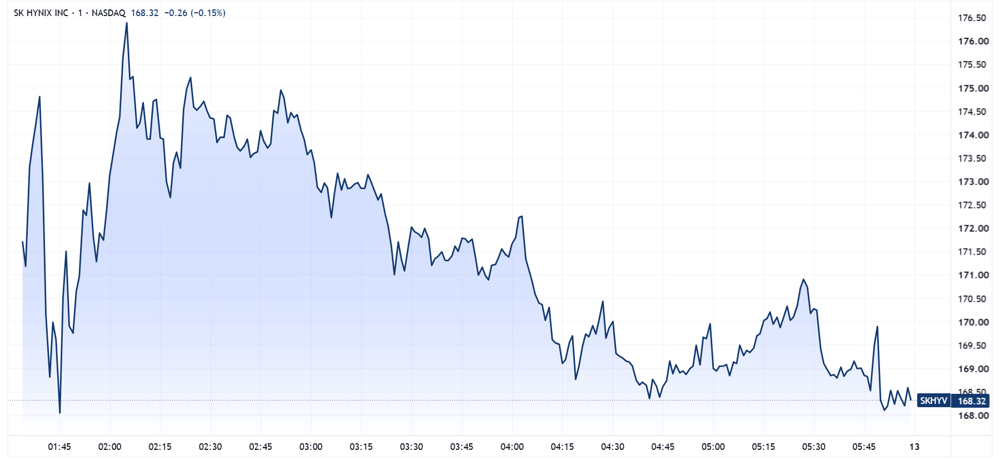

SK Hynix jumps 13% in record Nasdaq debut

[8:43 am] SK Hynix’s American depositary receipts closed 13% above their offering price on their first US session, capping the largest ever first-time share sale by a foreign company.

-

ADRs closed at US$168.01, up 13% from the US$149 pricing but below the US$170 open, with more than 106 million ADRs traded, around half the outstanding ADRs

-

The US$26.5bn offering was more than seven times oversubscribed and ranks as the third-largest debut share sale ever

-

ADRs trade at roughly a 16% premium to the Seoul-listed common stock, narrowing the valuation gap with Micron, helped by restrictions on converting the Korean shares

-

Baillie Gifford, Coatue Management and Situational Awareness Partners took about US$5bn as cornerstones, US$2bn below the filing maximum

-

Proceeds will fund additional capacity and EUV lithography machines, with management and Gabelli Funds flagging tight memory supply-demand into at least 2028

-

Chairman Chey Tae-won signalled scope for further US share issuance if returns and demand hold, though leveraged ETFs continue to amplify volatility, with Seoul shares logging more than 50 sessions of 5%-plus moves this year versus about 37 last year

SK Hynix Nasdaq-listed ADRs, intraday chart (Source: TradingView)

Wall Street dealers turn net short on corporate bonds for first time

[8:41 am] Primary dealers are running an aggregate net-short position in corporate bonds for the first time on record, prompting debate over whether it signals caution or simply a structurally changed market.

-

Dealers hold a net-short position of roughly US$4bn in corporate bonds so far this year, versus a peak average inventory of US$16bn over 2017, per Crisil Coalition Greenwich data going back to 1998

-

The short is concentrated at the long end, around US$13.7bn short in bonds maturing in five years or more, offset by a US$9.66bn long in shorter-dated debt, where prices are more exposed to yield shifts

-

Credit spreads sit near multi-decade lows at around 0.74 percentage points over Treasuries, leaving dealers thinly paid to hold credit risk amid sticky inflation and elevated rates

-

Strong demand from insurers, pensions and money managers reinvesting higher-yielding coupons has left dealers unable to keep bonds in inventory

-

Electronic execution now handles 49% of investment-grade and 32% of high-yield trades, up from 8% and 2% a little over a decade ago, letting dealers match client flows without warehousing risk

-

Lazard flags the position’s asymmetry, warning that if spreads tighten dealers forced to cover into thin supply could amplify a rally

Source: Bloomberg

SK Hynix US listing spawns leveraged ETF wave

[8:37 am] SK Hynix’s record US debut is triggering a rush of leveraged ETF launches, importing the volatility-amplifying bets that already dominate its Seoul trading.

-

At least six leveraged products launch next week offering two times the daily return of SK Hynix’s US-listed ADRs, with some issuers preparing inverse products for bearish bets, from ProShares, Leverage Shares and Rex Shares

-

SK Hynix, Samsung and the leveraged products tracking them account for more than 70% of trading value in Korea’s $4.3 trillion equity market, a concentration that has whipsawed the Kospi

-

CSOP’s Hong Kong-listed SK Hynix leveraged product is the world’s largest of its kind, holding more than US$16bn in assets before a recent share price slide

-

Bloomberg Intelligence warns US investors may face the same tracking errors seen in Hong Kong, as issuers struggle to source shares and hedge when demand outstrips inventory

-

JPMorgan Asset Management’s John Cho flagged the launches as a sign of late-cycle, momentum-driven retail behaviour rather than a healthy development

Source: Bloomberg

Good morning!

[8:31 am] ASX 200 futures are up 43 pts (+0.49%).

The overnight session in a nutshell:

-

S&P 500 (+0.42%), Dow (+0.29%), Nasdaq (+0.29%), Russell 2000 (-0.49%)

-

Major US benchmarks mostly higher, with the S&P 500 and Nasdaq booking a second straight weekly gain amid relatively broad gains for Tech, Defensives and Materials

-

SK Hynix stormed its Nasdaq debut, opening around 14% above its offer price after raising US$26.5bn, the largest ever US listing by a foreign company

-

Iran declared the Strait of Hormuz closed over the weekend after a third US strike wave, reviving oil supply fears just as crude had settled back near its lowest since the war began

-

Brent up 4.9% in early trade on Monday to US$78.90 a barrel, gold trading sharply lower, down 0.9% to US$4,083/oz

{kind=link}